What can Betshare tell us about a betting market?

Posted 22nd January 2017

It's often assumed that the efficiency of a betting market, that is to say the accuracy of its betting prices, is a reflection of the preferences of a wise betting crowd and the bookmaker's attempts at balancing or equalising the action on either side of a result. But is this necessarily the case? Without information about how many people are actually betting on particular propositions, and what money they are staking, we can't be entirely sure how the market is being formed and managed by the bookmaker. Fortunately, Pinnacle.com, recognised as the world's sharpest odds setter, publishes data on the percentage of customers placing bet via its twitter feed. This article analyses a sample of those percentages, called betshares, for the football total goals betting market to see what clues it might offer.

Trawling through the last year or so of betshare tweets from Pinnacle.com, I have collected a sample of 200 football matches with the goal line (typically between 2 and 3.25) and the percentage of bets placed on both Over and Under. Also shown are the opening and closing odds for those lines (taken from Oddsportal.com). Matches include those from the English Premier League, German Bundesliga, Spanish La Liga, Champions League, Europa Cup and international competitions including friendlies.

75% of matches witnessed a preference for betting on the Over (betshare greater than 50%) whilst the average Overs betshare was 62%. This bias towards betting over the bookmaker's goal line is something that other sources have reported, including betting social media platform Pyckio and sports betting analytics website SportsInsights. If we were to assume a priori that the expected betshare should be evenly distributed between Over and Under, such a bias is highly statistically significant (2-tailed, 2-sample paired t-test) with about a 10 in a quintillion probability that this difference over 200 matches would have arisen by chance.

What are the implications of this bias? Well, firstly, if we were to assume that all bettors betting Over and Under wager roughly the same stakes on average, the bookmaker would be heavily exposed to losses should the Over win. The corollary is that the bookmaker should shorten his odds on the Over dramatically in an attempt to balance the action on both sides of the betting line. For example, for fair odds of 2.00 for both over and under 2.5 goals, a 62% betshare for the Over would necessitate odds shortening to 1.61, with a corresponding lengthening to 2.58 for the Under. Clearly, such a dramatic odds shift would create an obvious and significant value opportunity for Under bettors, which in turn would influence the betshare. Speaking to SportsInsights, Scott Cooley, an Odds Consultant for the market-setting Bookmaker.eu, makes the case that this is not what actually happens at all.

"I think a common misconception is that books are feverishly trying to balance out the sides. Yes, in a perfect world it'd be nice to have equal action on both sides so our risk is zero, but that obviously doesn't happen for every game. We will certainly accept the unbalanced action if we feel we're in the right position. Sometimes we're right, and sometimes we're wrong."

Perhaps bookmakers are willing to be part of the action when required.

Furthermore, how likely is it that bettors targeting Over or Under are staking in the same general way? Pinnacle.com have hinted that where betshares are heavily skewed in favour of one side over the other, the implication is that those betting on the smaller betshare option are doing so in larger volumes. Referring to three pointspread betshares for a Major League Baseball playoff series between Kansas City Royals and Baltimore Ravens which saw betshare percentages as low as 5%, they had this to say:

"Money moves our markets, so if the market hasn't moved, the amount of money on each side should be fairly even. In a case where only 5% of bets are on one side and 95% on the other, the total amounts wagered on either side are very likely similar, in which case the average bet on the 5% side is nothing short of massive. It's well-known that one habit of sharp (big) bettors is to fade the public; when you recognize that Pinnacle offered the best price in the market on the Royals' opponents in all three games, you understand why the public was betting against Kansas City, and what those sharps saw to keep the market in check."

Evidently, then, where bettors on difference sides of the line are staking in different way, the bookmaker is still able to manage his liabilities without having to offer too much value to the sharper bettor.

SportsInsights have suggested that squares, those recreational punters who will more usually stake small to moderate sizes, have a tendency to pound the Overs. Sharps, by contrast, stake bigger and are more likely to focus on the Unders given the potential for value that might exist. Just how much value might arise in the Unders as a consequence of a preferential bias towards Overs, and does it cause systematic movements in the betting odds when it's present. Let's take another look at Pinnacle's football total goals betting market.

There is little point in analysing returns from betting on the Unders market from just 200 matches, since profitability can easily arise simply by chance. With average margins of 2.9% and 2.4% for opening and closing odds respectively, just a small deviation away from expectation could see a blanket betting of the Unders return a profit. Assuming an average bet win expectation of 50%, a 10,000-run Monte Carlo simulation confirms that we could expect to return some profit after 200 wagers over a third of the time. We need a much bigger sample to eliminate the role of chance. Analysing the over/under 2.5 goals opening betting odds from Pinnacle.com for 83,634 football matches played from 2007 to 2016 showed returns of 97.2% and 96.4% for blanket Overs and Unders betting respectively. The difference between the two is not statistically significant (p-value = 0.22, 2-tailed 2-sample paired t-test). Such evidence would appear to confirm that despite any preference towards Overs betting, Pinnacle at any rate are not offering up any meaningful value to sharps looking to exploit the cognitively biased preferences of squares.

But these are opening odds, I hear you cry. Perhaps we'll see some value appear by the time the market closes. That's possible, so let's take another look at our original sample of 200 matches, and see if there is any meaningful movement on those odds which correlates with the size of betshares. To ensure we're comparing like with like between opening and closing prices, first we must remove the margin, since the opening market attracts a slightly bigger margin than the closing one. For simplicity I've assumed equal weight is applied to both Over and Under, probably a fair assumption give the rough equality in price and the small size of the overall margin. Doing this yields the following figures.

|

Opening market |

Closing market |

|

Over |

Under |

Over |

Under |

| Average win expectation |

49.97% |

50.03% |

49.54% |

50.46% |

| Average odds |

2.02 |

2.01 |

2.03 |

1.99 |

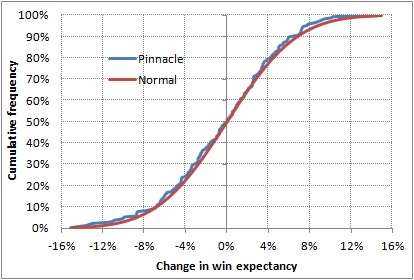

To all intents and purposes there is, on average, almost no odds movement at all, and what little there is, is actually against the Overs which are preferred by the majority of bettors. Unsurprisingly, the difference between the Under and Over betting odds in this 200-match sample is not statistically significant (p-value = 0.26, 2-tailed 2-sample paired t-test). Furthermore, plotting the distribution of individual odds movements as percentage win expectation changes on a cumulative distribution chart (positive change implies closing odds shorter than opening odds) reveals them to be effectively normally or randomly distributed.

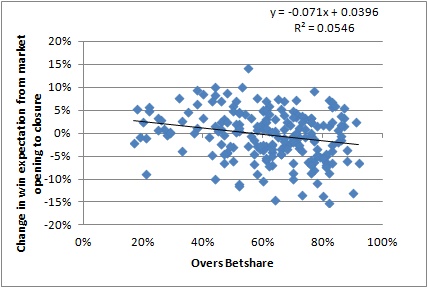

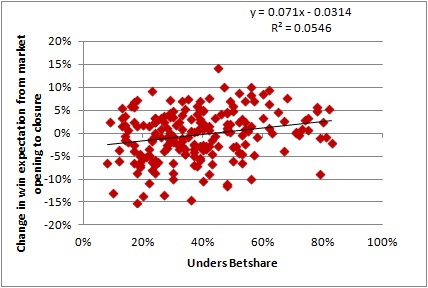

Finally, we can see if the odds movement correlates in any way with the size of the betshare. A priori, if a preference towards the Overs was causing a shortening of their odds towards market closure we should see this as a positive correlation in a scatter plot; the greater the betshare, the greater the predicted increase in win expectation as implied by the betting odds. In fact, we see the opposite: the greater the betshare for the Overs option, the more it will actually lengthen between market opening and closure. The reverse is of course true for the Unders. This would appear to contradict the suggestion that the pounding of Overs by squares creates value opportunities for sharps in the Unders. On the contrary, on average the price for an Under shortens by closing for those with the least interest.

Whilst this correlation is statistically significant (p-value = 0.001, linear regression), its strength is very weak with little more than 5% of the variance in the betshares accounting for the variance in the odds movement (r-squared = 0.055). Given that the price movements largely appear to be random anyway, this can hardly come as a surprise. With the average shift between opening and closing prices for the most disproportionate betshares barely 5%, on average at least there would seem be little theoretical advantage to be gained knowing betshare information.

What does all this mean for the way a bookmaker like Pinnacle manages its total goals betting market? Without actual turnover data we are still very much in the dark about how liabilities are being managed precisely. We still don't know to what extent so-called sharps betting Unders are out-staking their square counterparts pounding the Overs. And we still don't know how much 'action' the bookmaker is prepared to accept himself and how often. Nevertheless, the insignificant difference between returns for blanket betting Overs versus Unders, the apparent random nature of odds movement between market opening and closure, and the very limited relationship between betshare percentage and price movement would seem to point to their being limited scope for developing a consistently viable betting system based on betshare knowledge alone.

What is not in doubt is that bettors, as an aggregate, are heavily biased towards betting on the Overs market. In collecting the data for 200 football matches, I also collected Pinnacle betshare data for other sports as well, including Tennis and the four major American sports football, hockey, baseball and basketball. Across the 134 games for all sports, the same bias prevailed: 62% versus 38%. Individually, whilst sample sizes were small, the same preference for Overs betting existed for each: NHL 59%/41%; MLB 64%/36%; NFL 55%/45%; NBA 64%/36%; Tennis 65%/35%. Perhaps the most intriguing question is why bettors prefer the Over? In my recent book Squares & Sharps I proposed a simple hypothesis: loss aversion.

In prospect theory, loss aversion refers to the tendency for people to strongly prefer avoiding losses in comparison to acquiring gains. According to two Israeli psychologies, Amos Tversky and Daniel Kahneman who developed the theory, losses are as much as twice as psychologically powerful as gains in decision-making environments under uncertainty. One of the key principles of prospect theory is our irrational weighting of low and high probabilities, placing too much emphasis on the former and not enough on the latter. Previously I have suggested that this irrational weighting could be a contributing factor towards the favourite-longshot bias in moneyline/fixed betting odds. In an Over/Under betting market, our aversion to losses might be explained in the following way (taken from my book).

Consider the nature of an over/under bet. By its very structure, at the start of a match, one side, the Under, is automatically a winner, and remains so until such time as enough goals (or points) are scored to transform it into a loser. In contrast, the Over starts out as a loser and remains so until such time as enough goals (or points) are scored to transform it into a winner. In light of what prospect theory informs us, bettors, conceivably, may prefer the possibility of seeing a loser transformed into a winner rather than the other way around. If losing hurts about twice as much as winning is enjoyed, the bias in favour of 'losers into winners' over 'winners into losers' would seem to make sense. Daniel Mateos, Pyckio's co-founder, revealingly explains why he, too, suffers from an Overs bias.

"I don't want to be caught, that is, if you go for the Overs, you feel positive feelings with every goal; if you go for the Unders you feel negative feelings with every goal. It's stupid, but that is how I feel, and I am supposed to be a more rational bettor than average."

Conceivably, those bettors who intentionally fade squares by focusing on the Unders have given more thought to their betting and will more readily resist the temptation to be influenced by this psychological bias. If that is true, we might also expect such disciplined bettors to contain a disproportionately greater number of sharps than those merely betting on gut instinct. Arguably, then, such a subset of bettors would show larger staking volumes, thereby providing the mechanism described by Pinnacle.com to account for a relatively unchanging market despite heavily skewed betshares. Nevertheless, whatever the reality of actual betting volumes and bookmaker liability, the odds layer in an Over/Under betting market appears to be very reluctant to give any advantage away at all.

|